UK Gambling Tax and Horse Racing: The Tax You Don’t Pay and the One Bookmakers Do

UK gambling tax on horse racing is one of the most frequently misunderstood aspects of the betting market. The headline fact is simple: punters in the UK do not pay tax on their winnings. Whether you win £10 or £10,000, the amount that hits your account is the amount you keep. No income tax, no capital gains tax, no deduction of any kind. The bookmaker, however, pays tax — and that tax shapes every aspect of the product you interact with, from the odds you are offered to the promotions like NRNB that are available to you.

Understanding how UK gambling tax works is not about calculating your own liability (you don’t have one). It is about understanding the financial structure within which bookmakers operate — and why that structure produces the offers, margins, and betting experience that you see when you open your account.

The tax you don’t pay — and the one bookmakers do. Here is how it works and why it matters.

Remote Gaming Duty: The Tax Bookmakers Pay Instead of You

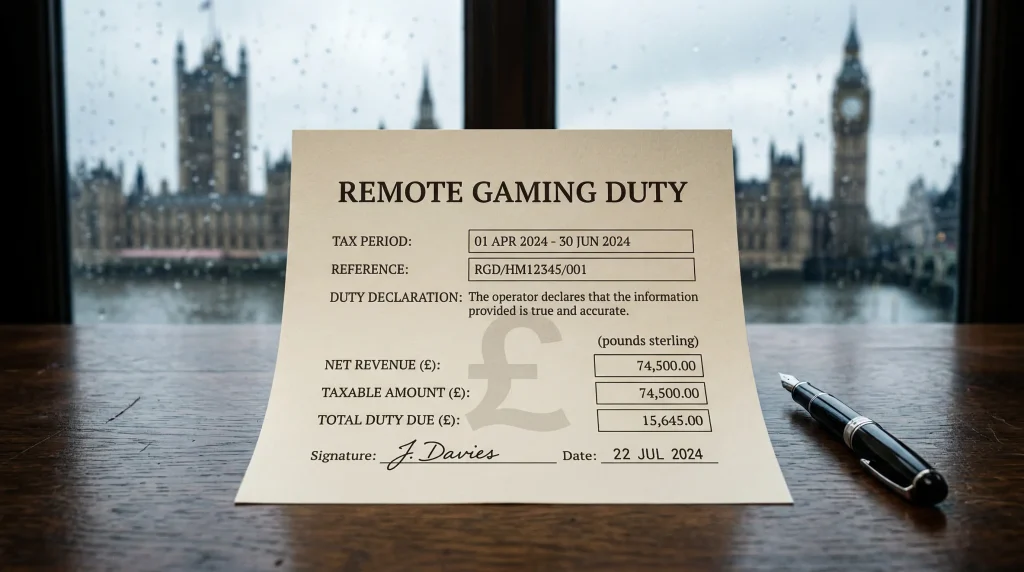

Since 2014, the UK has levied Remote Gaming Duty (RGD) on all licensed gambling operators offering services to UK customers. RGD is charged at 21% of the operator’s gross gaming yield — the difference between amounts staked by customers and amounts paid out in winnings. This replaced the previous system where the “point of supply” determined taxation, and it brought offshore operators into the UK tax net for the first time.

RGD applies to all forms of remote (online) gambling, including horse racing, football, casino, and other sports. For horse racing specifically, the tax sits alongside General Betting Duty (GBD), which applies to retail (high street) bookmakers at 15% of gross profits on general bets. The combined effect is that bookmakers pay a significant percentage of their horse racing revenue to HMRC.

The scale of this revenue is substantial. HMRC collected £1,163 million in Remote Gaming Duty in the financial year 2026/25, a 13% increase on the previous year, according to GOV.UK statistics. Machine Games Duty contributed a further £609 million. Together, the various gambling duties generate over £3 billion annually for the Treasury — making the gambling industry one of the more significant sources of tax revenue outside the mainstream income, VAT, and corporation tax streams.

For punters, the practical relevance of RGD is indirect but real. The 21% charge on gross profits is a cost that bookmakers must recover through their pricing. It is embedded in the margins: the odds you are offered are set to generate gross profits that cover operating costs, RGD, the betting levy, and a return for shareholders. A higher tax rate means the bookmaker needs wider margins to remain profitable, which translates into less generous odds, tighter promotional budgets, or both.

Before 2001, UK punters themselves paid a 9% tax on their stakes. The abolition of that tax — replaced by the bookmaker-side duty — was a landmark change that made British betting significantly more attractive for consumers. The current system means your £10 bet goes entirely into the market; no portion is deducted for tax. But the bookmaker’s side of the equation is taxed heavily, and that cost flows through to you via the pricing structure.

How Gambling Tax Shapes Bookmaker Promotions Like NRNB

Every promotional offer a bookmaker runs — NRNB, BOG, extra places, enhanced odds — is a cost. That cost reduces the operator’s gross profits, which in turn reduces the base on which RGD is calculated. In accounting terms, promotional spending comes off the top: a £50 NRNB refund reduces the bookmaker’s GGY by £50, and the RGD charge on that £50 disappears.

This creates a subtle incentive alignment. The bookmaker pays less tax when it runs more promotions, because promotions reduce gross profits. This does not mean promotions are tax-driven — the primary motivation is customer acquisition and volume generation — but the tax treatment means the net cost of a promotion to the bookmaker is lower than the face value of the refund. A £50 NRNB refund costs the bookmaker approximately £39.50 after the RGD saving, not £50.

Matt Zarb-Cousin, co-founder of Gamban, argued that horse racing should be treated differently within the affordability checks framework, noting that the implementation of checks has been inconsistent across operators. His point touches on the same structural issue: the regulatory and tax environment in which bookmakers operate directly shapes the promotional products they offer to punters. Tighter regulation and higher taxes compress the margin available for promotions; a more permissive framework allows wider promotional spending.

The ongoing affordability debate is relevant here. If affordability checks reduce the number of high-value customers who bet on horse racing, the bookmaker’s gross profits from racing decline. Lower gross profits mean lower RGD payments, which reduces Treasury revenue — creating a feedback loop where stricter regulation produces less tax income. The government’s challenge is to calibrate the regulatory framework in a way that protects consumers without eroding the tax base that gambling duties provide.

UK vs Other Countries: Tax on Horse Racing Bets

The UK’s approach to gambling tax — zero for punters, duty on operators — is not universal. Different countries take very different approaches, and the structure of the tax system directly affects what kind of betting experience is available to customers.

In the UK, the return from betting turnover to the racing industry is approximately 0.6%, delivered through the statutory levy. In Ireland, where a similar bookmaker-side model applies, the return is roughly 1.5%. In France, where pool betting (PMU) dominates and the state operates the monopoly, around 8.6% of turnover flows back to racing. In the United States, where pari-mutuel systems prevail for horse racing, the figure is approximately 14.5%. In Japan, the return is 16.6%.

These figures, compiled by the Thoroughbred Daily News and subsequent analyses, illustrate a spectrum. At one end, the UK offers the most consumer-friendly tax treatment (no tax on winnings) but returns the least to the sport. At the other, Japan and France tax betting more heavily at the point of consumption but channel far more money into racing infrastructure, prize funds, and breeding.

For UK punters, the trade-off is favourable in the short term: you keep every penny you win, and the competitive bookmaker market ensures a wide range of promotions and tight margins. The long-term question is whether the low rate of return to racing — 0.6% versus double-digit percentages in other major jurisdictions — is sustainable as the market contracts. If turnover continues to decline and the levy cannot keep pace with racing’s funding needs, the quality of the product you bet on may gradually diminish, even as the tax treatment of your winnings remains the most generous in the world.

The tax you don’t pay — and the one bookmakers do — shapes every aspect of the UK betting market. The odds, the promotions, the NRNB offers, the competitiveness of the market: all are products of a tax system that loads the cost onto operators and leaves customers untouched. That system has made UK horse racing betting among the most accessible and consumer-friendly in the world. Whether it can sustain the sport it depends on is a different question — and one that the turnover figures are beginning to answer.